A few minutes searching with Kasasa Care and GoodRx can save you up to 80% on the over-the-counter medications you regularly reach for.

Between mailers, sales letters, and all the fine print in between, choosing the right Medicare plan can seem like an overwhelming task. Even though it seems like all you have to do is decide between two simple options — Original Medicare or Medicare Advantage — there’s actually a lot more that goes into making your final choice.

If you’ve been exploring your Medicare options for a while, you might be wondering — do you need additional coverage if you stick with Original Medicare? If you think you do, what’s the difference between an additional Medigap plan and the all-in-one alternative, Medicare Advantage? To help you get a better idea, we’re breaking down the differences in coverage, monthly costs, and care options so you can make a more confident decision.

What does Original Medicare cover?

Medicare Part A and Part B are what make up Original Medicare. Medicare Part A is hospital insurance, which covers inpatient hospital stays, care in a nursing facility, hospice care, and some health care. Medicare Part B is medical insurance, which covers certain doctors’ services, outpatient care, labs, medical supplies, and preventive services.

If you stick with Original Medicare, you’re covered if you need to go to the hospital or have a checkup with your primary physician. If you need prescription drug coverage or would like any additional coverage, you can enroll in Medicare Part D and/or Medigap for an extra, supplemental cost through a private insurance company.

You can enroll in Original Medicare (or Parts A and B) directly from the government — in some cases, you’re automatically enrolled on your 65th birthday.

Think of Original Medicare as basic coverage — you’ll need to be enrolled in Parts A and B if you’d like to switch to a Medicare Advantage plan. If you’d like to add on any additional coverage, like Medigap and Medicare Part D, you do not need both parts to enroll — one or the other is enough. Once you’re signed up and have your shiny new Medicare card in hand, you’ll then be able to break down the additional coverage that works best for your needs and budget. (We’ll walk you through those differences next.)

This all might seem a little different than what you might be used to with your previous health coverage, but rest assured, you’ll be able to enroll in the kind of coverage that best fits you.

What is Medigap (or Medicare Supplement)?

Medigap, or Medicare Supplement, is extra health coverage you can buy from a private company to pay for health costs that are not covered by Original Medicare. You’ll need to be enrolled in Original Medicare in order to enroll in this type of supplemental coverage. While this cost varies depending on your plan, it is designed to help fill the “gaps” in Original Medicare, since an Original Medicare plan covers most — but not all — healthcare costs, like co-pays, coinsurance, and deductibles. Some policies even cover medical care when you travel outside of the U.S., as long as it is a type of care covered by Original Medicare.

Medigap policies are designed to lower out-of-pocket costs for Original Medicare — not provide additional coverage, or cover things outside of Original Medicare. So if you opt for this plan, you’ll just have Part A (hospital insurance) and Part B (medical insurance), but your overall costs will end up being much lower, thanks to Medigap.

Here’s how it works:

-

Your Original Medicare will pay its share for covered care costs.

-

Then, your Medigap policy will pay its share. (Either the remaining amount or most of the cost.)

Some Medigap policies have covered prescription drugs in the past, but now they do not. If you want prescription drug coverage, you can join a Medicare Part D (prescription drug) plan in addition to Medigap. Medigap policies also have monthly premiums, too — so be sure to shop around to get the plan that meets your budget.

What is included in a Medicare Advantage plan?

Medicare Advantage, also called Medicare Part C, is privatized, all-in-one health insurance. This is similar to the health coverage you might have had in the past — but with some plans, you might get even more perks. (Usually at no added cost!)

These perks are referred to as supplemental benefits, and they are not usually covered by an Original Medicare plan (and Original Medicare plans with supplemental Medigap). Your health and wellness isn’t just about doctor’s visits — it’s a lifestyle, and a Medicare Advantage plan can help make those healthier habits an integral part of your daily life. Some of the most common benefits include:

-

Routine services: think vision insurance, dental insurance, and even hearing aids — what once used to be additional coverage you had to enroll in can be bundled with Medicare Advantage.

-

Wellness services: gym memberships and fitness programs are usually covered, so you can stay active.

-

Clinical services: these are things like routine foot care or acupuncture and chiropractic services, because even the slightest joint pain can have a big impact on your daily life.

-

Support services: while home meal deliveries and non-emergency transportation might not be a priority when comparing your health plan options, these benefits provide peace of mind — and make your recovery time after a hospital stay or surgery that much easier.

To switch to Medicare Advantage, you must already have Medicare Part A and Part B, and also live within the service area of your Medicare Advantage plan. And when you’re shopping around, just know that not every Medicare Advantage plan has the option of Part D. So if you’re looking for prescription drug coverage, make sure the plans you’re interested in have it included.

How does your geographic location affect getting supplemental Medicare coverage?

You might be thinking — does my address really matter? When it comes to your Medicare options, it actually does.

If you choose to stick with Original Medicare, you have access to care anywhere in the United States as long as the provider accepts Medicare. So if you travel a lot (maybe you’ve finally decided to get that RV you’ve always dreamed of!) or have a vacation home elsewhere, Original Medicare might be the smarter choice in the event of an emergency or illness.

Medicare Advantage, on the other hand, is based around networks of providers. These are usually contained to your geographic area. This also means that if you live in a more rural area, your provider choice could be pretty limited. You could still get the care you needed if you were on the road or in another place, but there’s a big chance you could end up paying more with an out-of-network provider.

And something important to note: if your retirement plans include travel abroad, neither Original Medicare nor Medicare Advantage covers your healthcare in another country. You may be able to buy supplemental insurance that includes travel coverage, however.

What is the difference in provider availability between Medicare plans?

A big difference (and usually the ultimate deciding factor for many) between Original Medicare with a Medigap supplement plan and Medicare Advantage is the provider network availability.

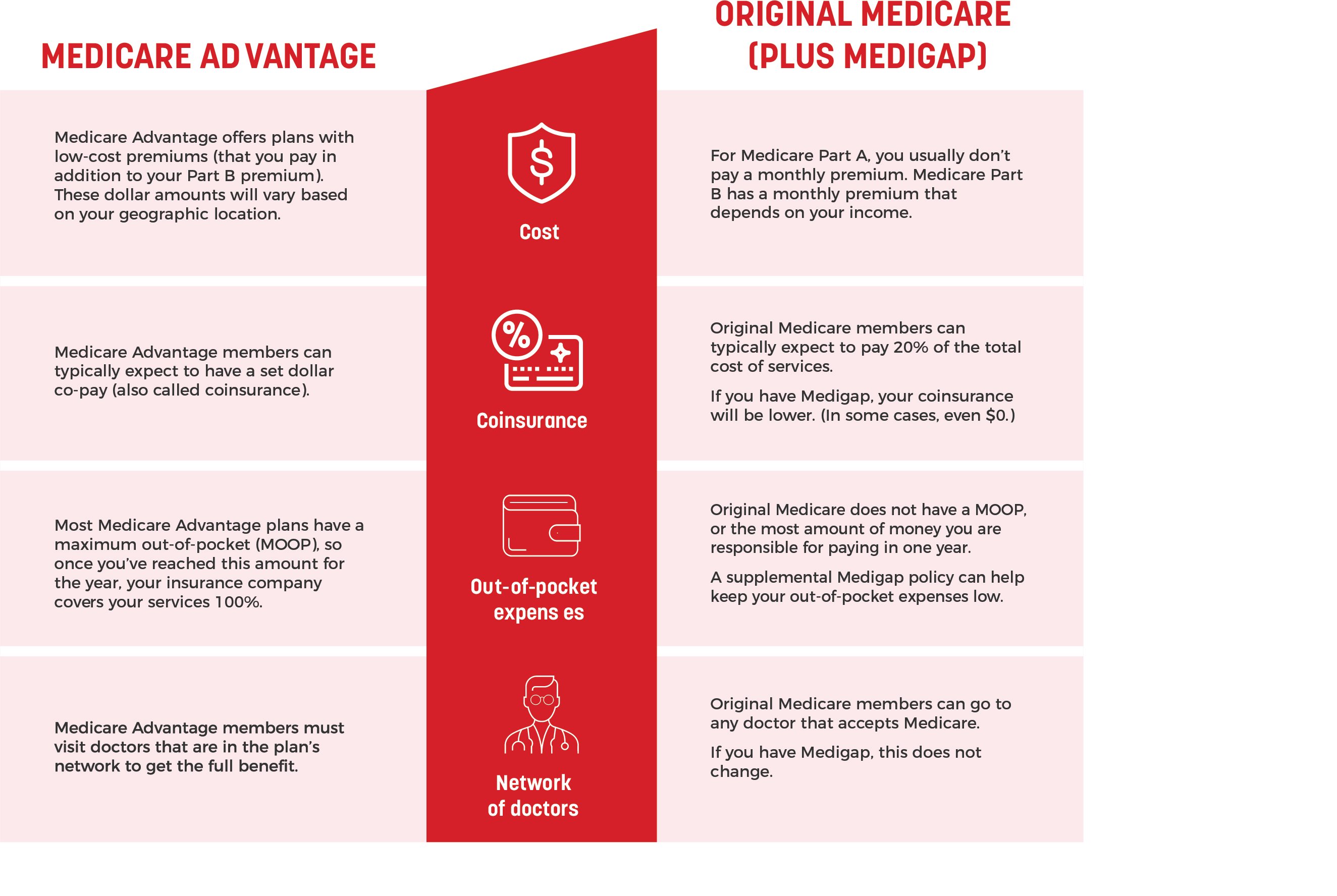

With Original Medicare, you can go to any doctor that accepts Medicare. And this is good news! It’s estimated that 93% of non-pediatric doctors say they accept Medicare. So if you like having options (or, you know, are living the ultimate #retirementgoals in an RV), Original Medicare might be the way to go. Plus, with a Medigap plan, you'll have even lower out-of-pocket costs.

And again, with Medicare Advantage, members must visit doctors that are in the plan’s network to get the full benefit. If you needed care outside of your network or have other provider preferences, your plan won’t pick up the tab in most cases — you’ll be responsible for most (or all) of the cost.

What is the difference in monthly premium costs between Medicare plans?

When you start crunching numbers, there are a few key differences between Medicare plans as far as care costs. One plan is not necessarily cheaper than the other — it truly all depends on how much care you need, and your financial situation. However, both plans have premiums, co-pays, deductibles, and coinsurance — all things you’ve been used to with your previous health insurance coverage.

For Medicare Part A, you usually don’t pay a monthly premium if you (or your spouse) paid enough in Medicare taxes while you were working. Medicare Part B does have a standard monthly premium amount — for 2021, this is around $148, depending on your income. So if you decide to go with Original Medicare, you can expect to pay around that much per month.

If you have Original Medicare and want to add on Medicare Part D (prescription drug coverage) and/or Medigap, this will be an additional monthly cost. But because both of these plan types are available through private insurance companies, this cost varies.

On the other hand, Medicare Advantage offers plans with low-cost premiums that are often as low as $0. Depending on your geographic location, these dollar amounts will vary.

What is the difference in the cost of care between Medicare plans?

With the monthly cost considered, let’s break down how much it will cost you when you actually have to use your coverage. Generally speaking, Original Medicare members will pay 20% of the total cost of services with no limit to out-of-pocket spending — but if you add on a Medigap plan, it can help cover most (or all) of the remaining cost.

Medicare Advantage members typically have a set dollar co-pay, with a maximum out-of-pocket limit (or MOOP) per calendar year. A co-pay is also called coinsurance, which is the percentage you pay for a covered health service. And with Medicare Advantage, your co-pays for doctor’s visits and hospital stays count toward the MOOP. But because you must enroll in these plans through a private insurance company, these costs vary.

If you like knowing exactly how much your care will cost — and if you need more of it in general — a Medicare Advantage plan might be for you. If you’re still active and healthy, and don’t foresee any surgeries or non-routine doctor’s visits in your future, Original Medicare might be the better option.

Before you make your choice, it’s a good idea to grab a calculator and a good-old fashioned pencil and paper. What might seem like the obvious, cost-effective choice might actually not be the right one for your unique situation. It all depends on the care you need, your preferences, and your budget, too.

How do you switch from Original Medicare to Medicare Advantage?

To switch between Original Medicare and Medicare Advantage, you have to be eligible in the first place. People who are 65 years of age or older, or if you have certain disabilities, are eligible for Medicare. You may be automatically enrolled into Medicare Part A on your 65th birthday — think of it as a gift to you from the United States government, a welcome letter and all! If you’d like Part B, you must elect for it — here’s how (and when).

If you’re not automatically enrolled, you have the opportunity to sign up during your Initial Enrollment Period, also called IEP. This is a seven-month period of time when you can enroll in Original Medicare for the first time. It begins three months before your birthday, lasts throughout your birth month, and ends three months after your 65th birthday.

If you’d like to enroll in Medicare Advantage, you must:

-

Already have Medicare Parts A and B.

-

Have checked to make sure you live in the plan’s service area.

-

Do not have end-stage renal disease.

There are only certain times of the year when you can either enroll in or switch your Medicare plans. It’s similar to the Open Enrollment period you might have experienced while on a regular health insurance plan or your employer’s health plan. They are:

-

The Annual Election Period, in which you can change your plan or enroll in Medicare Advantage. Your benefits will go into effect on January 1 of the upcoming year. This usually happens from October 15 to December 7 each year.

-

A Special Enrollment Period, which is when certain qualifying life events occur, like retirement, losing employer-covered insurance, or if you move out of your plan’s service area.

-

The Open Enrollment Period, which is a time for those that are already enrolled in a Medicare Advantage plan to change to a different plan. You can also switch back to Original Medicare during this time. This usually happens from January 1 to March 31 each year.

If you have other coverage currently, either through your employer, union, or other benefits administrator, make sure to speak with a trusted representative about making the switch to a Medicare plan. In some cases, joining a Medicare Advantage plan might cause you to lose your current coverage, which could also mean a coverage loss for any dependents or your spouse, too.

The seven things to consider when choosing a Medicare plan

We know that Medicare is, well, a lot. Now it’s time to think about where a plan and your needs align. To help you get started, here are seven things to consider:

-

Cost. Make sure you understand — based on your current and estimated future care needs — how either Medicare plan can keep your out-of-pocket expenses low.

-

Coverage. How well does either plan cover the services you need?

-

Other, supplemental coverage. Do you need Medigap to help with Original Medicare costs? Or would you rather get an all-in-one approach?

-

Prescription drugs. Do you have recurring and/or expensive prescriptions and need Medicare Part D?

-

Doctor and hospital choice. Are you okay with a smaller network of providers, or does the freedom to choose have a higher priority?

-

Quality of care. Are you satisfied with your current medical care? Which plan is most similar?

-

Travel. Have you been counting down the days to hitting the road (in that RV!), heading to the beach, or hauling luggage overseas?

We hope this roundup offered some clarity into your Medicare choices. Hopefully you have a better idea of which plan can best meet your specific needs. To put it simply, there is no one “better” choice — it all comes down to what you value and the amount of care you need.