Consumers have higher expectations when it comes to checking accounts today. With the majority of people researching a checking account online before they open one, they know they don’t have to settle for the one that is closest to home.

What Consumers Hate About Their Checking Account

According to the CFPB, the most common complaints filed about an institution's service and products are accessibility issues, customer support issues, and fees.

We'll look at actual quotes from consumer complaints in an attempt to understand where institutions go wrong and what can be done about it.

Fees

"Without proper notifications, [Name removed] started a maintenance fee on my account... Before charging the fee they did not even inform me of the fee is coming in proper ways..."

It shouldn’t be a surprise that consumers hate fees. But most accept them, thinking it’s just the cost of banking. While 92% of consumers claim to be aware of the fee structure at their bank, 1 in 4 still feel scammed by bank fees.

Here’s the good news for community financial institutions. According to the 2015 Consumer Banking Insights study, when it comes to fees, megabank customers are twice as likely to feel scammed by bank fees compared to community bank and credit union account holders. In fact, JPMorgan Chase, Bank of America, and Wells Fargo collected more than $6.4 billion in ATM and overdraft fees from customers last year.

What fees do consumers detest the most?

- 31% said monthly service fees

- 26% said ATM fees

- 20% said overdraft fees

- 15% said minimum balance fees

Accessibility / Technology

"For the 3rd time, my bank is withholding my paycheck entirely. The only reason they give me is that they are holding it because they are allowed to do so for 14 days."

According to a CFPB study, 28% of complaints against financial institutions were dealing with difficulties withdrawing or depositing funds. The two main causes of this issue are not-understood policies and inadequate technology. In the above example, it might be within the institution's policy to withhold the funds, and they might have a very good reason to do so, but what caused the issue with the consumer is that s/he wasn't expecting it. Being kept in the dark on the policy, the reason behind the withholding, and transparency around how to resolve this issue only escalated the situation.

"I deposited a cashier's check from a local bank into my personal checking account at [Name removed] via the ATM. I usually go into the branch, but was in a hurry and used the ATM to deposit my check - big mistake!"

Consumers expect omnichannel service that allows them to manage their finances and resolve any issues on the device they are currently on, be that mobile, desktop, social media, phone, or in-branch. Another aspect of this expectation is the delivery of equal quality service across devices.

Lack of Transparency

"I had a couple of auto pay transactions and an unexpected expense arose and it caused my account to go negative. Merchants send ACH through 2-3 times and it caused over {$200.00} overdraft fees. The bank wasn't willing to refund the fees. I understand the initial fee but if a merchant attempts the transaction 2-3 times I'm not able to stop it."

Here is a common example: Consumers believe that when debiting their account, transactions will be processed in the order which they were incurred. If a consumer's account has a balance of $20 and they make three $5 purchases and one $20 purchase in the span of a day (in that order), they expect the three $5 purchases to be resolved first, incurring an overdraft fee on just the $20 purchase. However, a more common practice is to resolve the $20 charge first, which would cause the consumer to overdraft on all of the $5 charges. To consumers, this seems dishonest and as if the policy is rigged to cause them to fail.

What Consumers Want Instead

Rewards

With the right account, consumers can get rid of those top two fees they hate. Completely free checking accounts don’t charge monthly service fees, and some accounts (like Kasasa Reward Accounts) offer ATM fee refunds. In fact, for 71% of U.S. adults, features like free checking, ATM fee refunds, and access to the latest banking products are more important when choosing where to bank than the institution that provides them.

What else do consumers want? They’re looking for rewards like ATM refunds and cash back on their accounts. In fact, 78% of consumers said cash back options are at least somewhat important when choosing a financial institution (Among Millennials, 91% identified cash back options as at least somewhat important!).

Omni-channel Experiences

The industry has mistakenly framed the common debate about branches as an "either/or" scenario; Do consumers want to bank in a branch OR do they want mobile. The reality is that consumers want to do business where and when it is easiest for them.

Partnership and Education

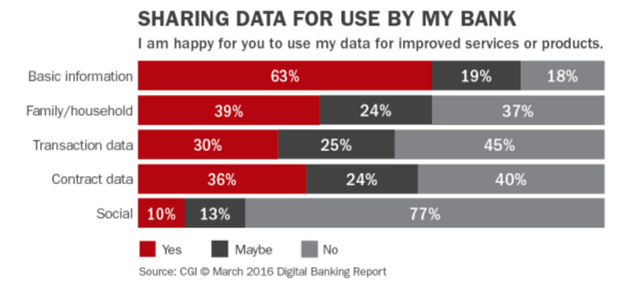

Consumers report being very open to receiving advice and guidance from their institutions. A study by Accenture found that 48% of consumers expect specialized treatment and that 33% of consumers who left a business did so due to lack of personalization. Consumers expect businesses to use collected data to make personalized recommendations on how to better their financial standing.

Source: https://thefinancialbrand.com/58063/personalization-in-banking-digital-research-study/

Source: https://thefinancialbrand.com/58063/personalization-in-banking-digital-research-study/

Only 25% of consumers feel their bank looks out for their financial being. To be transparent, you need to educate consumers on your institution's policies before they experience an issue. As we saw above, half of the issue is the fee and half is For more advice, check out this post on handling fee-related complaints.

How You Can Give Them What They Want

To become the institution of choice for consumers in your market, community banks and credit unions need to look at their products to make sure they align with what people want from a checking account. They want to be rewarded for using their account, not charged. By giving out rewards instead of collecting fees, you’ll also be rewarded with loyal account holders for years to come.

*2015 Consumer Banking Insights Study