What separates Generation Y from X? And hey Gen Z and Gen A, welcome to the party! What’s the cutoff? How old is each generation? Are they really that different?

It’s easy to see why there is so much confusion about generational cohorts.

If you’ve ever felt muddled by this "alphabet soup" of names — you’re not alone. The real frustration hits when you realize that Millennial consumers represent the highest-spending generation in 2020 — with a projected $1.4 trillion tab.

And though their current wealth has been dragged down by not one but two “once-in-a-lifetime” economic crises during their most impactful career years, Millennials stand to inherit over $68 trillion from Baby Boomer and early Gen X parents by the year 2030, setting them up to potentially be the most wealthy generation in U.S. history.

Generation Z isn’t far behind, projected to hit $33 trillion in income by 2030 — that’s more than a quarter of all global income — and pass Millennials in spending power the year after. 3

And coming up last but not least is Generation Alpha, the name given by social analyst Mark McCrindle to the youngest children on the planet. By the year 2025 there will be nearly 2 billion members of Generation Alpha across the globe.

No matter how you slice the data, the younger generations have never been more critical to your financial institution’s future.

Unless you understand who they are and what they want, you won’t capture a dollar of their money.

People grow older. Birthdays stay the same.

A common source of confusion when labeling generations is their age. Generational cohorts are defined (loosely) by birth year, not current age. The reason is simple — generations get older in groups. If you think of Millennials as college kids (18 - 22), then not only are you out of date — you’re thinking of a stage in life, not a generation. Millennials are now well out of college, and that life stage is dominated by Gen Z.

Another example, a member of Generation X who turned 18 in 1998 would now be over 40. In that time, he or she cares about vastly different issues and is receptive to a new set of marketing messages. Regardless of your age, you will always belong to the generation you were born into.

The breakdown by age looks like this:

-

Baby Boomers: Baby boomers were born between 1946 and 1964. They're currently between 57-75 years old (71.6 million in the U.S.)

-

Gen X: Gen X was born between 1965 and 1979/80 and is currently between 41-56 years old (65.2 million people in the U.S.)

-

Gen Y: Gen Y, or Millennials, were born between 1981 and 1994/6. They are currently between 25 and 40 years old (72.1 million in the U.S.)

-

Gen Y.1 = 25-29 years old (around 31 million people in the U.S.)

-

Gen Y.2 = 29-39 (around 42 million people in the U.S.)

-

-

Gen Z: Gen Z is the newest generation, born between 1997 and 2012. They are currently between 9 and 24 years old (nearly 68 million in the U.S.)

-

Gen A: Generation Alpha starts with children born in 2012 and will continue at least through 2025, maybe later (approximately 48 million people in the U.S.)

The term “Millennial” has become the popular way to reference both segments of Gen Y (more on Y.1 and Y.2 below).

Sometimes labeled with the moniker “Zillennials”, those wedged at the tail end of Millennials and the start of Gen Z are sometimes labeled with this moniker — a group made up of people born between 1994 and the year 2000.

Originally, the name Generation Z was a placeholder for the youngest people on the planet — although Generation A has now taken over that distinction. However, in the same way that Gen Y morphed into Millennials, there is certainly a possibility that both Gen Z and Gen A may adopt new names as they leave adolescence and mature into their adult identities. While the label Gen A makes discussion easier, it may not be the last word on this group of humans.

Why are generations named after letters?

It started with Generation X, people born between 1965-1980. The preceding generation was the Baby Boomers, born 1946-1964. Post-World War II, Americans enjoyed newfound prosperity, which resulted in a "baby boom." The children born as a result were dubbed the Baby Boomers.

But the generation that followed the Boomers didn’t have a blatant cultural identifier. In fact, that’s the anecdotal origin of the term Gen X — illustrating the undetermined characteristics they would come to be known by. Depending on whom you ask, it was either sociologists, a novelist, or Billy Idol who cemented this phrase in our vocabulary.

From there on it was all down-alphabet. The generation following Gen X naturally became Gen Y, born 1981-1996 (give or take a few years on either end). The term “Millennial” is widely credited to Neil Howe, along with William Strauss. The pair coined the term in 1989 when the impending turn of the millennium began to feature heavily in the cultural consciousness.

Generation Z refers to babies born from the late 90s through today. A flurry of potential labels has also appeared, including Gen Tech, post-Millennials, iGeneration, Gen Y-Fi, and Zoomers.

While some say Generation Alpha is named for the first letter of the Greek alphabet and denotes the first of a series of items or categories, Generation Alpha may also just be an easy way to round the corner into a new alphabet.

Splitting up Gen Y

Javelin Research noticed that not all Millennials are currently in the same stage of life. While all Millennials were born around the turn of the century, some of them are still in early adulthood, wrestling with new careers and settling down, while the older Millennials have a home and are building a family. You can imagine how having a child might change your interests and priorities, so for marketing purposes, it's useful to split this generation into Gen Y.1 and Gen Y.2.

Not only are the two groups culturally different, but they’re in vastly different phases of their financial life. The younger group is just now flexing their buying power. The latter group has a more extensive history and may be refinancing their mortgage and raising children. The contrast in priorities and needs is stark.

The same logic can be applied to any generation that is in this stage of life or younger. As we get older, we tend to homogenize and face similar life issues. The younger we are, the more dramatic each stage of life is. Consider the difference between someone in elementary school and high school. While they might be the same generation, they have very different views and needs.

Marketing to young generations as a single cohort will not be nearly as effective as segmenting your strategy and messaging.

Why are generation cohort names important?

Each generation label serves as a shorthand to reference nearly 20 years of attitude, motivations, and historical events. Few individuals self-identify as Gen X, Millennial, or any other name.

They’re useful terms for marketers and tend to trickle down into common usage. Again, it’s important to emphasize that referring to a cohort only by the age range gets complicated quickly. Ten years from now, the priorities of Millennials will have changed — and marketing tactics must adjust instep. There are also other categories of cohorts you can use to better understand consumers going beyond age or generation.

Remember, these arbitrary generational cutoff points are just that. They aren’t an exact science and are continually evolving.

Whatever terminology or grouping you use, the goal is to reach people with marketing messages relevant to their phase of life. In short, no matter how many letters get added to the alphabet soup, the most important thing you can do is seek to understand the soup du jour for the type of consumer you want to attract.

What makes each generation different?

Before we dive into each generation, remember that the exact years born are in dispute, because there are no comparably definitive thresholds by which the later generations (after Boomers) are defined. But this should give you a general range to help identify what generation you belong in.

The other fact to remember is that new technology is typically first adopted by the youngest generation and then is gradually adopted by the older generations. As an example, 96% of Americans have a smartphone, but Gen Z (the youngest generation) is the highest user.

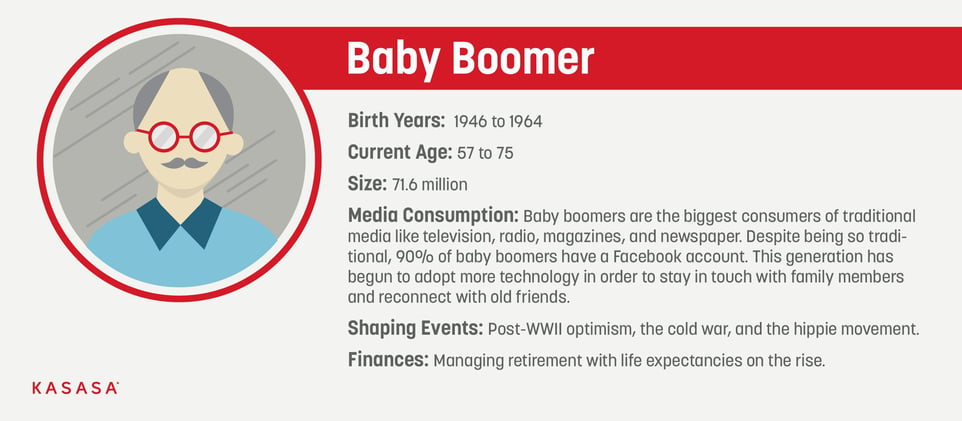

The Baby Boomer Generation

-

Boomer Birth Years: 1946 to 1964

-

Current Age: 57 to 75

-

Generation Size: 71.6 million

-

Media Consumption: Baby boomers are the biggest consumers of traditional media like television, radio, magazines, and newspaper. Despite being so traditional, 90% of baby boomers have a Facebook account. This generation has begun to adopt more technology in order to stay in touch with family members and reconnect with old friends.

-

Banking Habits: Boomers prefer to go into a branch to perform transactions. This generational cohort still prefers to use cash, especially for purchases under $5.

-

Shaping Events: Post-WWII optimism, the cold war, and the hippie movement.

-

What's next on their financial horizon: This generation is experiencing the highest growth in student loan debt. While this might seem counterintuitive, it can be explained by the fact that this generation has the most wealth and is looking to help their children with their student debt. They have a belief that you should take care of your children enough to set them on the right course and don't plan on leaving any inheritance. With more Americans outliving their retirement fund, declining pensions, and social security in jeopardy, ensuring you can successfully fund retirement is a major concern for Boomers.

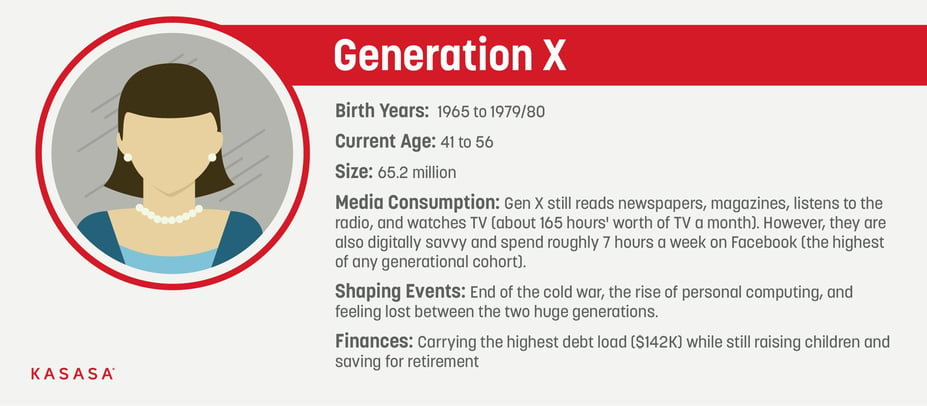

Generation X

-

Gen X Birth Years: 1965 to 1979/80

-

Current Age: 41 to 56

-

Other Nicknames: "Latchkey" generation, MTV generation

-

Generation Size: 65.2 million

-

Media Consumption: Gen X still reads newspapers, magazines, listens to the radio, and watches TV (about 165 hours' worth of TV a month). However, they are also digitally savvy and spend roughly 7 hours a week on Facebook (the highest of any generational cohort).

-

Banking Habits: Since they are digitally savvy, Gen X will do some research and financial management online, but still prefer to do transactions in person. They believe banking is a person-to-person business and demonstrate brand loyalty.

-

Shaping Events: End of the cold war, the rise of personal computing, and feeling lost between the two huge generations.

-

What's next on Gen X's financial horizon: Gen X is trying to raise a family, pay off student debt, and take care of aging parents. These demands put a high strain on their resources. The average Gen Xer carries $142,000 in debt, though most of this is in their mortgage. They are looking to reduce their debt while building a stable saving plan for the future.

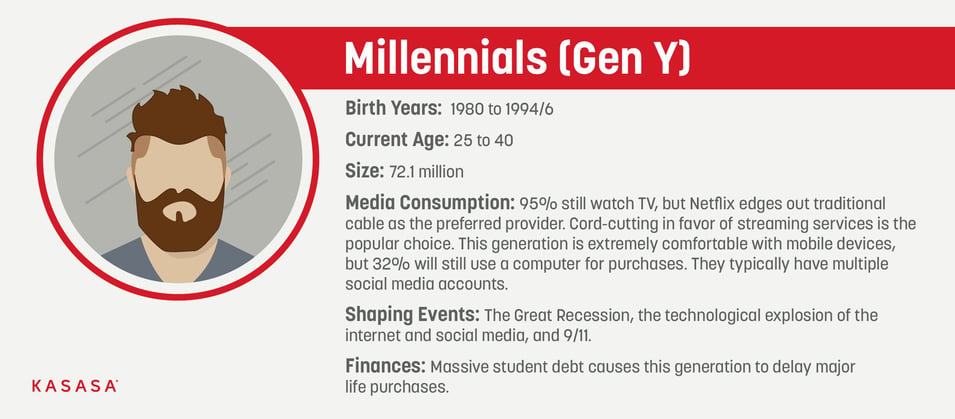

Millennials (Gen Y)

-

Millennial Birth Years: 1981 to 1994/6

-

Current Age: 25 to 40

-

Other Nicknames: Gen Y, Gen Me, Gen We, Echo Boomers

-

Generation Size: 72.1 million

-

Media Consumption: 95% still watch TV, but Netflix edges out traditional cable as the preferred provider. Cord-cutting in favor of streaming services is the popular choice. This generation is extremely comfortable with mobile devices, but 32% will still use a computer for purchases. They typically have multiple social media accounts.

-

Banking Habits: Millennials have less brand loyalty than previous generations. They prefer to shop products and features first, and have little patience for inefficient or poor service. Because of this, Millennials place their trust in brands with superior product history such as Apple and Google. They seek digital tools to help manage their debt and see their banks as transactional as opposed to relational.

-

Shaping Events: The Great Recession, the technological explosion of the internet and social media, and 9/11

-

What's next on their financial horizon: Millennials are powering the workforce, but with huge amounts of student debt. This is delaying major purchases like weddings and homes. Because of this financial instability, Millennials choose access over ownership, which can be seen through their preference for on-demand services. They want partners that will help guide them to their big purchases.

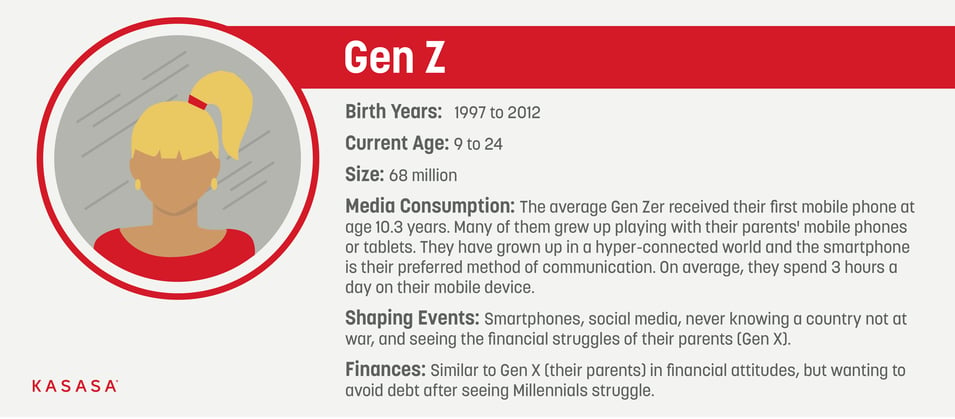

Gen Z

-

Gen Z Birth Years: 1997 to 2012

-

Currently Aged: 9 to 24

-

Other Nicknames: iGeneration, Post-millennials, Homeland Generation

-

Generation Size: 68 million

-

Media Consumption: The average Gen Zer received their first mobile phone at age 10.3 years. Many of them grew up playing with their parents' mobile phones or tablets. They have grown up in a hyper-connected world and the smartphone is their preferred method of communication. On average, they spend 3 hours a day on their mobile device.

-

Banking Habits: This generation has seen the struggle of Millennials and has adopted a more fiscally conservative approach. They want to avoid debt and appreciate accounts or services that aid in that endeavor. Debit cards top their priority list, followed by mobile banking.

-

Shaping Events: Smartphones, social media, never knowing a country not at war, and seeing the financial struggles of their parents (Gen X).

-

What's next on Gen Z's financial horizon: Learning about personal finance. They have a strong appetite for financial education and are opening savings accounts at younger ages than prior generations.

If you want to know more about Gen Z, check out this deep dive into their media consumption and banking habits.

Generation Alpha

-

Generation Alpha Birth Years: 2012 to 20256

-

Currently Aged: 0 to 9

-

Other Nicknames: None that have stuck. Often the nickname centers on a defining event or characteristic.

-

Generation Size: 48 million and growing

-

Media Consumption: Alphas are being raised in homes with smart speakers and devices everywhere; technology is built into everyday items. Many of them attended school virtually thanks to the global pandemic and are gravitating toward online learning with programs such as Khan Academy, Prodigy, and IXL. Many have even had a digital presence since before they were born, with their Millennial parents creating social media handles for their infants.

-

Banking Habits: Although some of the oldest Alphas may have accounts such as Greenlight, they do not have defining banking habits. They’re digital natives that will expect fully integrated, personalized consumer experiences. Based on current data, it appears that Alphas will be one of the most highly educated and wealthy generations. It is not clear if their banking habits will be influenced by their parents (i.e. “my parents bank here, so do I”) or by other factors.

-

Shaping Events: Global pandemic, social justice movement, Trump-era politics, and Brexit.

-

What’s next on Generation Alpha’s financial horizon: As digital natives who view the world through a collection of screens, Alpha’s will be even more disconnected from the idea of cash. They will likely first encounter money as a number on a screen and spend it through apps and other forms of ecommerce.

Do generations use technology differently?

Younger generations have often led older Americans in their adoption and use of technology, and this largely holds true today.

Although Baby Boomers may trail Gen X and Millennials on native technology usage, the rate at which Boomers expand their use of technology is accelerated.

In fact, Boomers are far more likely to own a smartphone than they were in 2011 (68% in 2019 vs. 25% then).

Are generations the best way to categorize consumer behavior?

Knowing generational trends is important, as they can unveil similar attitudes and behaviors among consumers who experienced world events at the same life stage as their cohorts. And it doesn’t hurt to understand these age groups since marketing tools and audience segmentations generally include age as a factor.

But the generations don’t tell the whole story and their behaviors can be hard to lock down. After all, every generation grows up. So. can you rely on age ranges alone? Here's what we think.

Do generations bank differently?

Absolutely, and for several reasons.

-

Each generation has been in the workforce for different lengths of time and accumulated varying degrees of wealth.

-

Baby Boomers have an average net worth of $1,066,000 and a median net worth of $224,000.

-

Gen Xers average net worth is around $288,700, but the median is $59,800.

-

Millennials have an average net worth around $76,200, but their median net worth is only $11,100.

-

Gen Z's average net worth is difficult to report on since so much of the generation has no net worth or career as of yet.

-

Each generation is preparing and saving for different life stages; be that retirement, children's college tuition, or buying a first car.

-

Each generation grew up in evolving technological worlds and has unique preferences in regard to managing financial relationships.

-

Each generation grew up in different financial climates, which has informed their financial attitudes and opinions of institutions. However, in the past year, the COVID-19 pandemic has become the great equalizer, as all generations have had to adapt to a new way of banking and living.

How are these banking differences appearing in the marketplace?

Ease of use vs. personal service.

If you think bots are taking over the world, you might be right. But for Millennial and Gen Z consumers, this isn’t necessarily a bad thing. In fact, according to a recent Adobe Analytics study, 44% of Gen Z and 31% of Millennials have used a banking chatbot to answer their questions. And before you think that must be a terrible user experience, over half of both groups who actually used a chatbot said the experience was better than talking to a real person.

However, for more complicated banking tasks, even the younger generations prefer the added assistance of a human representative.

Security still comes first, always. But each generation has their own priorities.

When choosing a new place to bank, “security” was the top-rated concern across Gen Z, Millennials, Gen X, and Boomers. “Reputation” (also known as your brand) finished second for both Gen Z and Millennial consumers.

However, for Gen Z and Boomer consumers, branch locations was the second most popular result, with “reputation” close behind. Younger consumers still care about branch locations but weigh it around the same level as an institution’s digital and app services.

For Generation X, digital and app services were edged out by in-person support. For Baby Boomers, banking local was more important.4 However, before you write off the importance of your online and mobile banking for these consumers…

Technology isn’t just for younger generations anymore.

The trend has long been for each new generation to adopt digital and mobile banking services more readily. But the COVID-19 pandemic has turned on a new wave of late-adopters who now bank digitally, too.

According to a recent Zelle survey, now 82% of seniors age 55+ are banking online more frequently — with 61% and 55% turning to social media and mobile banking more frequently too.5

That lines up closely with the start of the Baby Boomer demographic (currently ages 57 to 75). And while only time will tell how lasting this shift to digital tools and services will be, the more positive your digital experience, the more likely you are to extend your digital reach with this generation.

Today, older generations are behaving more like younger generations. And if you want to succeed in tomorrow’s market, you already need to meet these younger generations where they are. Now is the time to extend your brand of great service beyond the branch.

1 SOURCE: https://www.5wpr.com/new/research/5wpr-2020-consumer-culture-report/

5 SOURCE: https://www.zellepay.com/sites/default/files/2020-06/Senior_Polling_FINAL.pdf